It’s currently the wild west out there. Remember that private markets follow the public markets. In the next 6-12 months, startup valuations will be coming back to normal. There will be down rounds (i.e., when companies raise money at lower valuations), wide-spread layoffs as companies miss their earnings targets relative to their lofty valuations, and some companies will even close up shop. However, that doesn’t mean startups are destined to fail. Many companies are fairly valued and have raised enough money to operate in the shadows of the public markets for the next few years.

More than ever before, it’s imperative that you scrutinize the business model and underlying metrics of whatever company you’re thinking about joining.

If you’ve been paying attention to public markets since the meme stock craze that started in early Covid, then you’ve seen or participated in the wild roller coaster ride that is the public markets. Over the past 6 months, tech stocks have seen their share prices slashed dramatically. Companies like Robinhood, Stitch Fix, Snowflake, and more had their valuations cut in half in only a few short months. However, it’s not just retail investors that are feeling the pain. Byron Deeter, a partner at Bessemer Venture Partners, the oldest venture fund in the world, recently mentioned that the median stock in his basket of subscription software stocks is down 53% over the same time period. Similarly, hedge funds are at their lowest net-exposure to technology stocks in a decade.

If we look at the companies mentioned above, it’s not pretty:

Similarly, if we look with a wider aperture, the decline is just as bad — an entire index is down more than 30% in just 6 months. Below I charted an S&P 500 tracking ETF vs Wisdom Tree Cloud Computing ETF, a well known ETF that tracks high-growth Software and Cloud stocks:

Yikes. However, If we step back from the past 6 months and look at these ETFs on a longer time horizon, you’ll see a huge bull market in the shape of “up and to the right”.

So what happened?

There were a few things that contributed to the legendary Covid-enabled stock market run of the roaring 20s:

The pull forward of Digital Transformation across industries

Low interest rates enabling institutional investors to seek risk-adjusted haven in higher-growth asset classes like technology

Capital abundance via stay-at-home orders, government stimulus’, etc.

“End of the World Hysteria” in the form of cheap stock prices

Nearing the end of Covid (hopefully), everything has changed:

The pull forward of Digital Transformation across industries

Low interest rates enabling institutional investors to seek haven in higher-growth asset classes like technology

Capital abundance via stay-at-home orders, government stimulus’, etc.

End of the World Hysteria in the form of cheap stock prices

Now, we are feeling the repercussions of those two years of upside through tightening monetary policy (rising interest rates), a return to “normal”, a potential world war, and crippling inflation, culminating in a technology-stock bloodbath. In fact, we are at pre-Covid lows for technology multiples — 2 years of gains wiped clean!

Like I mentioned earlier, private markets trail public markets.

Private Markets: How Did We Get Here?

When it comes to valuation, it’s important to understand that it’s both art and science. In public markets, a company’s stock price is beholden to quarterly earnings calls, making public market investors very disciplined on their entry-price, almost scientifically so. One quarter the company could post positive results and the stock shoots up 10%. The next quarter, the company could give poor guidance for future growth and the stock dives 20%. In private markets, VCs are betting on future growth and have the benefit of long time horizons. The stock price of a private company does not fluctuate the way a public company’s price does. Private company valuation is art. Investors and founders negotiate on a valuation during each fundraising round, looking more and more like science as the company moves from Series A > IPO.

With that in mind, many startup companies are valued on a multiple of their revenue. Oftentimes, there isn’t intrinsic value that investors can analyze through a Discounted Cash Flow model or other valuation analyses the same way a public markets investor would. Instead, startup companies are valued based on their peer groups, revenue, and future growth. Unlike what you might have learned in Finance 101, fair-market valuation doesn’t exist in startup-land.

In a time with abundant uncertainty in public markets, more venture dollars being put to work than ever before, quicker capital deployment cycles for VCs, and competitive fundraising timelines, private-market investors are bidding up to pay expensive prices for future growth, culminating in wacky valuations and high priced expectations.

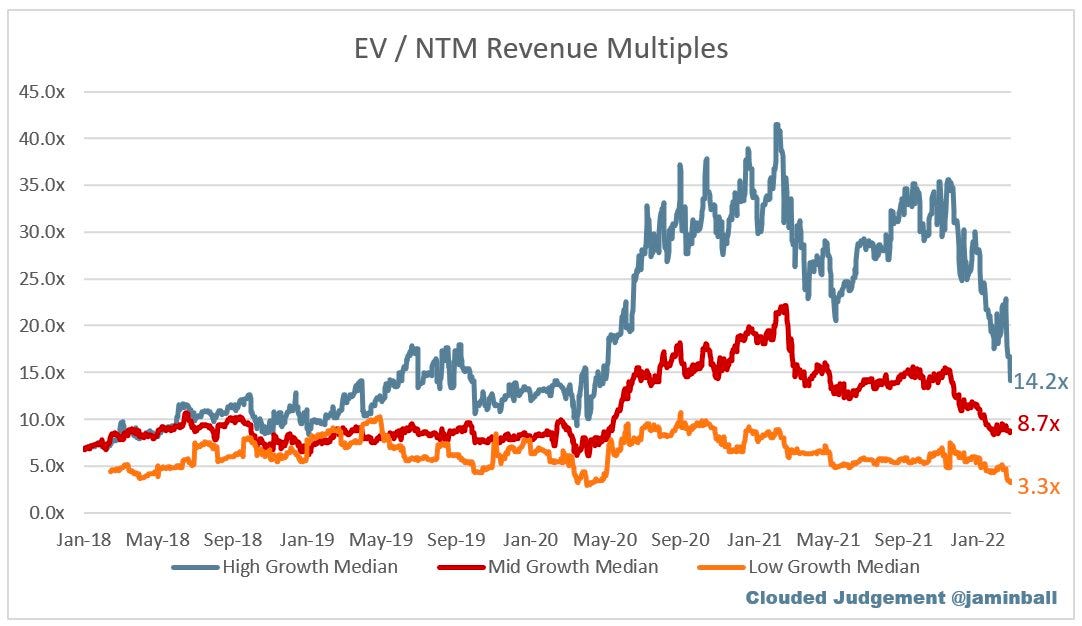

In the same way Covid accelerated public markets, the same was amplified for private markets. The median public markets high-growth revenue multiple (valuation barometer) in January 2020 was ~10x forward revenue. In May 2021, the multiple was ~40x. Today, multiples have retreated to pre-covid lows.

Still private market investors are/were willing to pay upwards of 100x for hot companies. But why?

Competition: Non-traditional investors are contributing to the surge in venture funding over the last 10 years. 77% of total dollars deployed are from hot money (e.g., hedge funds, private equity, mutual funds)

Exit Potential: Valuations paid by acquirers has continued to rise (Okta acquired Auth0 at a 37.5x multiple)

Increase in Capital: Venture investment was up 98% year-over-year

Fewer Strong Companies: Deals were only up 27% year-over-year

Despite an easy fundraising environment for founders, venture investors are willing to compromise on price and give inflated valuations to companies in order to win deals. While this might seem like a short term win, in the long term it is harder for companies to grow into massively inflated valuations. While startups don’t hold public earnings releases, private companies still share their financial performance with their board members and investors. If a company fails to hit revenue goals, but raised at a 100x valuation, that company is in for a rude awakening.

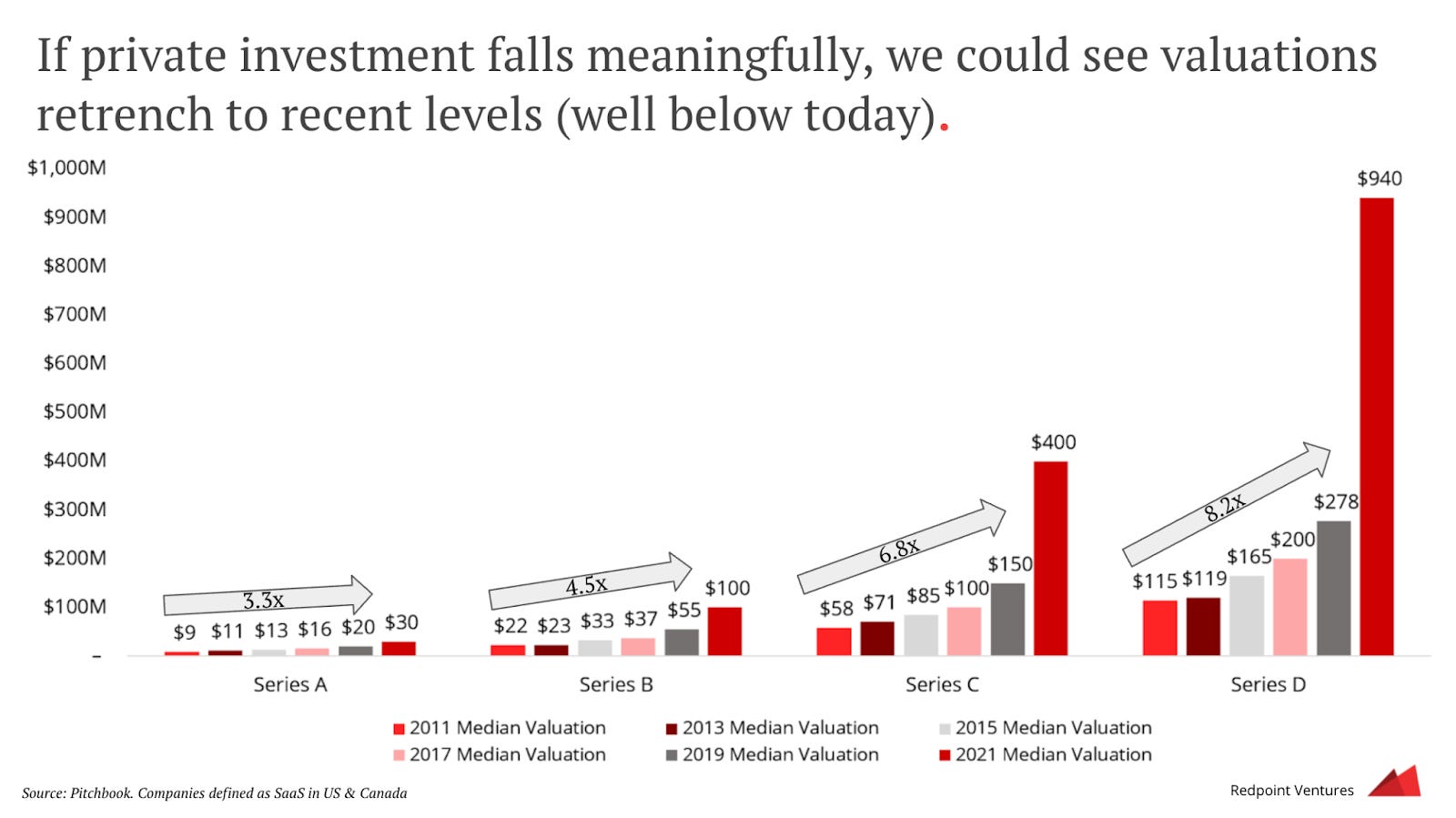

Below, I have included a chart from Logan Bartlett’s State of the Current Market presentation to illustrate just how inflated valuations are, and how far we have to drop to go back to “normal”:

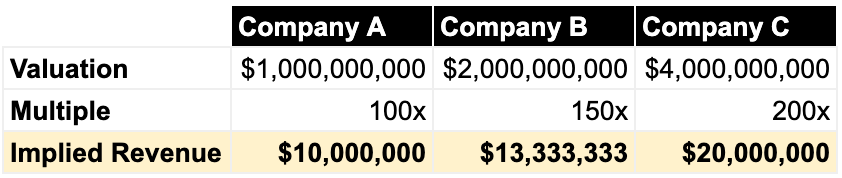

Similarly, I wanted to illustrate the sheer craziness of what the implied revenue is for these fundraising rounds:

When I joined my first startup company in 2019, we raised a $5M seed round at a $20M post-money valuation and I thought it was a huge sum of money. Today, software companies can raise at 100-200x revenue at $1B+ valuations! These valuations are crazy, especially when we look at historical multiples, but yet every day Techcrunch and Axios Pro Rata report new companies raising at monster valuations.

Private Markets: Where Are We Going?

The grim reaper is coming for many startups. Private companies are seeing investors pull back from high valuations, and over the next 6-12 months we’ll see down rounds, layoffs, and companies shut down. In theory, a market correction is not a bad thing — it just means the system is working properly. The companies that benefited from Covid’s Digital Transformation pull-forward will come back to reality (pre-Covid) while new fundraising rounds will be valued more fairly.

However, when it’s your job on the line, it will feel like the worst thing ever. That’s why it’s imperative to properly assess the companies you’re interviewing with to understand their trajectory, goals, valuations, metrics, and more.

The point of this essay is not to say that startups have suddenly become bad places to work, it just means you have to be careful about choosing the right one. If anything, startups are going to remain highly attractive places to work as short-term oriented equity investors call for public technology companies to become cash flow positive and cut costs. The main difference is that private technology companies have loaded up on cash and will be able operate in the shadows of the public eye while market conditions level-set to the absurdly strong performance being shown by today’s technology companies.

Closing Thoughts

Market cycles happen and are healthy. As public markets normalize and interest rates continue to rise, startup valuations will look more normal. I do not believe we will retrench to $1M seed rounds, but the days of 100x revenue will eventually come to an end.

The good news is, we are seeing fundamentally stronger companies being built today than ever before. Companies are posting insanely strong metrics and the appetite for technology within the enterprise and consumer landscape is as high as it’s ever been.

Maybe we’re seeing the end of an era, or perhaps this will be a blip on the radar. Too bad we won’t know until we’re looking back on it!