Like the Nike Swoosh

Fintech Finds: Check

Company Snapshot

Founded: 2019

Employees: 100

Funding: $120M

Stage: Series C

Locations: New York

Company Overview

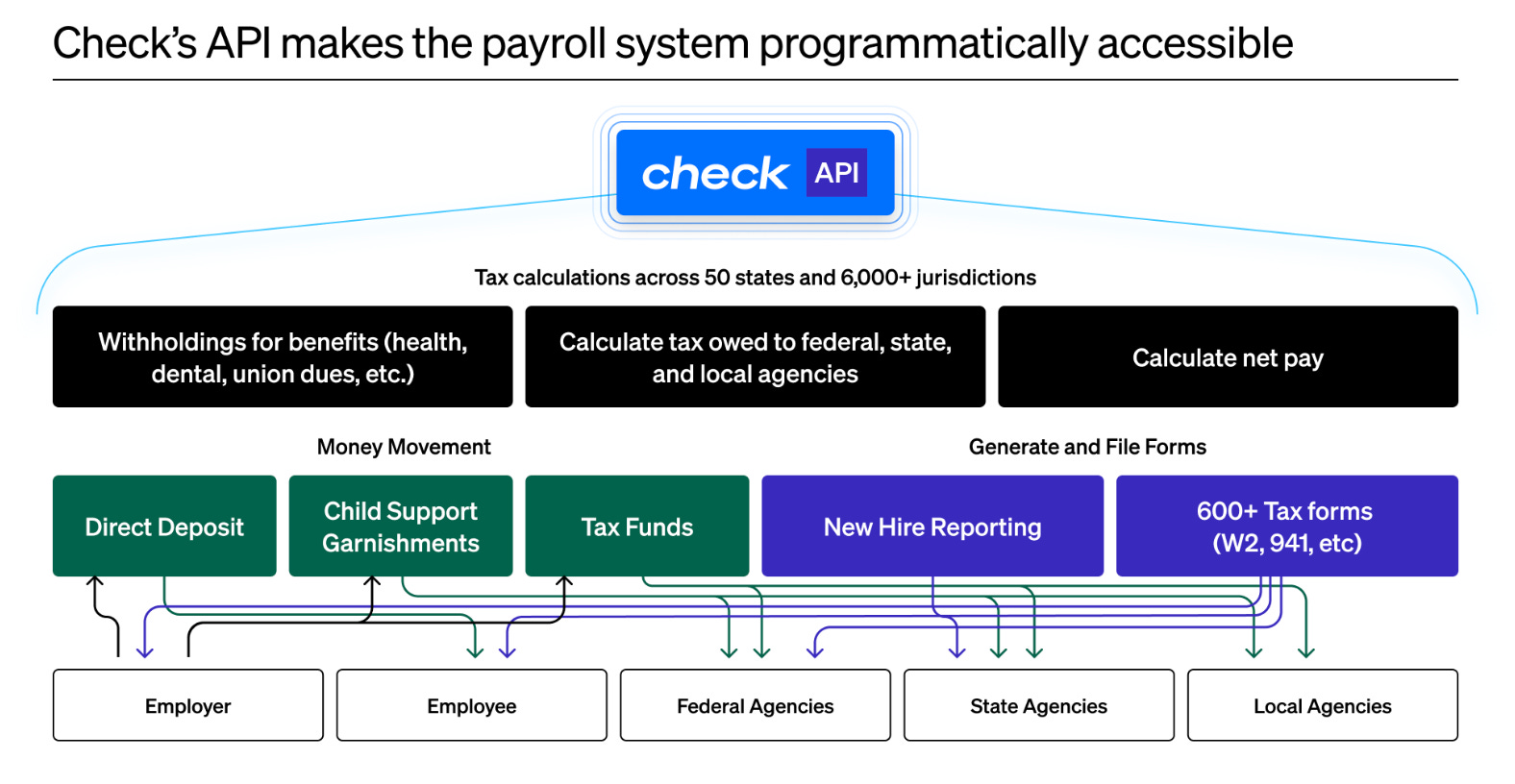

Check is an API for payroll.

Tell Me More

Check is building modern day payroll infrastructure. The company provides customers of all sizes the ability to leverage its payroll infrastructure for fast, efficient, and highly customizable payroll operations. In short, Check is building Stripe for payroll.

The Check API enables customers to pay employees on the back-end and build customizable front-end interfaces tailored to their unique payroll processing needs. The company allows customers to layer business rules for payroll processing including functionality for tax calculations, payment delivery, tax filings, and more. Check calculates employer and employee tax across more than 6,000 jurisdictions, accounts for benefits and deductions, keeps track of which employees are W-2 vs 1099, automatically updates the system of record as employment status’ change, and automatically generates and sends tax forms on behalf of the business, employee, and any contractors.

In essence, Check is building a performant API to automate one of the most boring but important aspects of fintech — paying your employees.

Market Opportunity

Payroll is purposely boring. There hasn’t been much innovation in the space. Legacy products like ADP are naturally sticky given the need for reliability and payment efficiency. Any mistake in payroll processing can have downstream ramifications to employees getting paid. Screwing up payroll is a big headache for companies and not something business owners want to mess with.

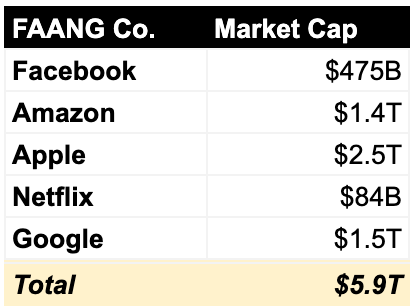

In 2020, there was over $8.9 trillion paid in US wages across all employment types. The market for payroll software is estimated to be growing at an 8.3% CAGR between 2020 and 2027. Check’s opportunity is exceedingly large. In 2020 dollars, the amount of payroll processed was ~1.5x larger than that of FAANG’s market cap.

Today, the market cap of payroll companies is greater than $150 billion, with ten companies valued at more than $10 billion.

One of the most intriguing opportunities for Check is the potential for legislative changes in employment status which could accelerate the need for flexible payroll software that would justify Check’s product-first approach across large enterprise customers.

For example, what would happen if Uber, Doordash, Lyft, Gopuff and the rest of the gig economy classified their workers as W-2 instead of 1099? These companies would need to reclassify their contractors to full-time employees within their payroll system. In many cases, the solution isn’t as simple as clicking a button the way it is in Check.

Why I like the company

Outside of modernizing payroll infrastructure, Check’s GTM strategy is fascinating. Realizing that it would be next to impossible to displace payroll behemoths like ADP, Oracle, and SAP that locked enterprise customers into large multi-year deals, Check strategically caters to B2B platforms, those operating scheduling, analytics, and benefits programs for other customers.

Basically, Check is a B2B2B payroll infrastructure machine. Since it’s increasingly difficult to build payroll systems, many of these B2B platforms integrate 3rd party payroll software into their own products, thereby allowing their customers to use ADP, Oracle, SAP, or Check payroll. However, many of these companies are startups themselves, servicing SMB customers who want flexibility in their own payroll operations and will choose Check (especially when they see the platform itself using Check).

Check benefits from SMB reliance on Platforms. The company has created positive feedback loops that allows it to service not only the large platforms that embed the API into their own products, but also the end customers who use Check to pay their employees. Landing a big fish deal with a platform provider aligns values across all vectors. Through just one platform deal, Check can aggregate hundreds of thousands of end users — an extremely efficient form of end customer acquisition.

Speaking of value-aligned products, Check earns its revenue through usage and subscription-based pricing. Traditionally, we’ve seen best in class net dollar retention and revenue growth coming from usage-based pricing products given that customers only pay for what they use and are not over-burdened guessing their capacity. For many end customers, they might not even know Check is processing their payroll. The only thing they care about is making sure their employees get paid.

Lastly, Check operates in a paradox — customers don’t necessarily like the products servicing the payroll market today, but the companies are still huge. ADP has a net-promoter score (NPS) of 0, but somehow a market cap of $93 billion. Similarly, Paychex has an NPS of 0, but a market cap of $44 billion. The market’s archaic functionality and poor customer experiences scores aligns perfectly to Keith Rabois’ formula for startup success:

Check’s Hiring Corner

Similar Companies

Reminder

As always, you can find the abbreviated list of companies we’ve already talked about here. Below are links to the previous posts